Where the regional housing market is shifting—and where it isn’t

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter. When assessing home price momentum, it’s important to monitor active listings and months of supply. If active listings start to rapidly increase as homes remain on the market for longer periods, it may indicate potential future pricing weakness. Conversely, a rapid decline in active listings could suggest a market that is heating up. Generally speaking, local housing markets where active inventory has returned to pre-pandemic levels have experienced softer home price growth (or outright price declines) over the past 24 months. Conversely, local housing markets where active inventory remains far below pre-pandemic levels have generally experienced stronger home price growth over the past 24 months. National active listings are on the rise (up 34% between September 2023 and September 2024); however, we’re still well below pre-pandemic levels (down 23% below September 2019). Here’s how the total September inventory/active listings compare historically, according to Realtor.com: September 2017: 1,308,607 September 2018: 1,301,922 September 2019: 1,224,868 September 2020: 749,395 (overheating during the Pandemic Housing Boom) September 2021: 578,070 (overheating during the Pandemic Housing Boom) September 2022: 731,496 (mortgage rate shock starts) September 2023: 702,430 September 2024: 940,980 Among the biggest inventory jumps: Florida. In Florida, the biggest inventory increases initially over the past two years were concentrated in sections of Southwest Florida. In particular, in markets like Cape Coral, Punta Gorda, and Fort Myers, which were hard-hit by Hurricane Ian in September 2022. This combination of increased housing supply from the damaged homes coming up for sale coupled with strained demand—the result of spiked home prices, increased mortgage rates, higher insurance premiums, and higher HOAs—translated into market softening across much of Southwest Florida. However, the inventory increases in Florida now expands far beyond SWFL. Markets like Jacksonville and Orlando are also above pre-pandemic levels, as are many coastal pockets along Florida’s Atlantic Ocean side. One reason for this is that Florida’s condo market is dealing with the aftereffects of regulation passed following the Surfside condo collapse in 2021. In August 2024, only four states had returned to or surpassed pre-pandemic 2019 active inventory levels. In September 2024, that number grew to seven: Tennessee, Texas, Idaho, Florida, Colorado, Utah, and Arizona. It’s nearly eight states if you include Washington State—which was just 35 homes below pre-pandemic levels. Other states likely to soon join that list include Oklahoma, Alabama, and Oregon. Why are Sun Belt and Mountain West markets seeing a faster return to pre-pandemic inventory levels than many Midwest and Northeast markets? One factor is that some pockets of the Sun Belt and Mountain West experienced even greater home price growth during the pandemic housing boom, which stretched affordability too far beyond local incomes. Once pandemic-fueled migration slowed and rates spiked, it became an issue in places like Colorado Springs and Austin. Unlike many Sun Belt housing markets, many Northeast and Midwest markets have lower levels of homebuilding. As new supply becomes available in Southwest and Southeast markets, and builders use affordability adjustments like buydowns to move it, it has created a cooling effect in the resale market. The Northeast and Midwest don’t have that same level of new supply, so resale/existing homes are pretty much the only game in town. Big picture: This year we’ve observed a softening across many housing markets as strained affordability tempers the fervor of a market that was unsustainably hot during the pandemic housing boom. While home prices are falling in some areas around the Gulf, most regional housing markets are still seeing positive year-over-year home price growth. The big question going forward is whether active inventory and months of supply will continue to rise and cause more housing markets to see outright price declines?

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

When assessing home price momentum, it’s important to monitor active listings and months of supply. If active listings start to rapidly increase as homes remain on the market for longer periods, it may indicate potential future pricing weakness. Conversely, a rapid decline in active listings could suggest a market that is heating up.

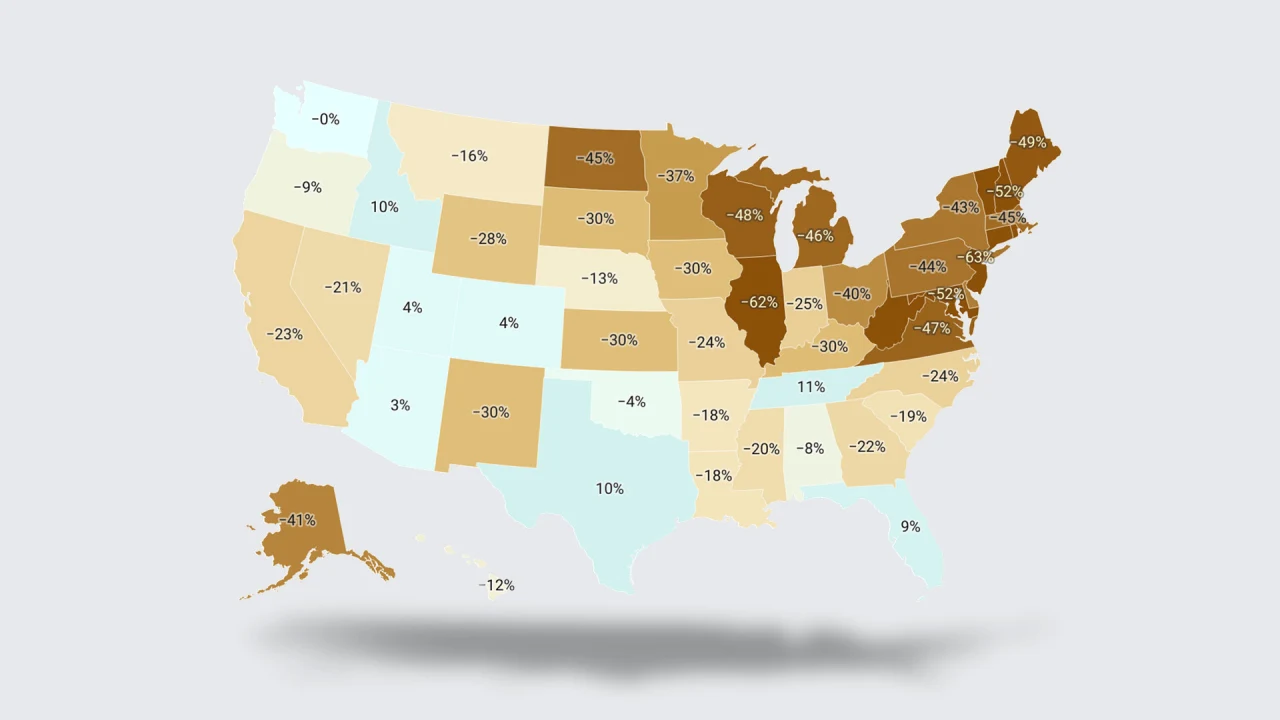

Generally speaking, local housing markets where active inventory has returned to pre-pandemic levels have experienced softer home price growth (or outright price declines) over the past 24 months. Conversely, local housing markets where active inventory remains far below pre-pandemic levels have generally experienced stronger home price growth over the past 24 months.

National active listings are on the rise (up 34% between September 2023 and September 2024); however, we’re still well below pre-pandemic levels (down 23% below September 2019).

Here’s how the total September inventory/active listings compare historically, according to Realtor.com:

September 2017: 1,308,607

September 2018: 1,301,922

September 2019: 1,224,868

September 2020: 749,395 (overheating during the Pandemic Housing Boom)

September 2021: 578,070 (overheating during the Pandemic Housing Boom)

September 2022: 731,496 (mortgage rate shock starts)

September 2023: 702,430

September 2024: 940,980

Among the biggest inventory jumps: Florida.

In Florida, the biggest inventory increases initially over the past two years were concentrated in sections of Southwest Florida. In particular, in markets like Cape Coral, Punta Gorda, and Fort Myers, which were hard-hit by Hurricane Ian in September 2022. This combination of increased housing supply from the damaged homes coming up for sale coupled with strained demand—the result of spiked home prices, increased mortgage rates, higher insurance premiums, and higher HOAs—translated into market softening across much of Southwest Florida.

However, the inventory increases in Florida now expands far beyond SWFL. Markets like Jacksonville and Orlando are also above pre-pandemic levels, as are many coastal pockets along Florida’s Atlantic Ocean side.

One reason for this is that Florida’s condo market is dealing with the aftereffects of regulation passed following the Surfside condo collapse in 2021.

In August 2024, only four states had returned to or surpassed pre-pandemic 2019 active inventory levels.

In September 2024, that number grew to seven: Tennessee, Texas, Idaho, Florida, Colorado, Utah, and Arizona. It’s nearly eight states if you include Washington State—which was just 35 homes below pre-pandemic levels.

Other states likely to soon join that list include Oklahoma, Alabama, and Oregon.

Why are Sun Belt and Mountain West markets seeing a faster return to pre-pandemic inventory levels than many Midwest and Northeast markets?

One factor is that some pockets of the Sun Belt and Mountain West experienced even greater home price growth during the pandemic housing boom, which stretched affordability too far beyond local incomes. Once pandemic-fueled migration slowed and rates spiked, it became an issue in places like Colorado Springs and Austin.

Unlike many Sun Belt housing markets, many Northeast and Midwest markets have lower levels of homebuilding. As new supply becomes available in Southwest and Southeast markets, and builders use affordability adjustments like buydowns to move it, it has created a cooling effect in the resale market. The Northeast and Midwest don’t have that same level of new supply, so resale/existing homes are pretty much the only game in town.

Big picture: This year we’ve observed a softening across many housing markets as strained affordability tempers the fervor of a market that was unsustainably hot during the pandemic housing boom. While home prices are falling in some areas around the Gulf, most regional housing markets are still seeing positive year-over-year home price growth. The big question going forward is whether active inventory and months of supply will continue to rise and cause more housing markets to see outright price declines?